What Does a Business Lawyer Actually Do?

Starting a business is exciting—but legal mistakes early on can create expensive problems later. If you have ever wondered what a business lawyer does and whether you need one, this guide breaks it down in plain language.

Whether you are forming an LLC, launching a startup, or growing an established company, a business lawyer helps you make smart decisions, stay compliant, and protect what you are building.

Have questions about your business? Use the contact form on this page or call (615) 747-7467 to schedule your initial consultation.

What Is a Business Lawyer?

A business lawyer, also called a business attorney, helps individuals and companies handle legal issues related to starting, operating, and growing a business. The goal is to reduce risk, prevent avoidable problems, and help business owners move forward with confidence.

Instead of waiting until something goes wrong, many business owners work with a lawyer to make better decisions from the beginning.

What Does a Business Lawyer Actually Do?

1. Helps You Start Your Business the Right Way

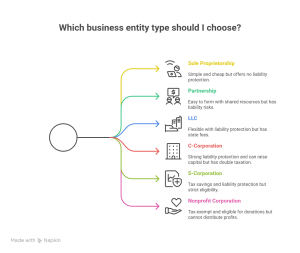

One of the first decisions you will make is choosing a business structure. Should you form an LLC or a corporation? The answer depends on your goals, taxes, ownership plans, and risk level.

A business lawyer can help by:

- Explaining your options in plain language

- Recommending the right structure for your situation

- Preparing and filing formation documents

- Drafting operating agreements, bylaws, and other foundational records

Getting this part right can help protect your personal assets and create a stronger legal foundation for your business.

Not sure which structure fits your business? Reach out through the contact form or call (615) 747-7467 for an initial consultation.

2. Drafts and Reviews Contracts

Contracts are part of almost every business relationship. Clear agreements can prevent confusion, protect expectations, and reduce the chance of expensive disputes.

A business lawyer can:

- Draft contracts tailored to your business

- Review agreements before you sign

- Negotiate stronger terms

- Help protect your rights and limit unnecessary risk

Common examples include client agreements, vendor contracts, partnership agreements, licensing agreements, independent contractor agreements, and employment-related documents.

Before signing your next contract, contact Moore Law PC through this site or call (615) 747-7467 to get it reviewed.

3. Keeps Your Business Compliant

Business owners have to deal with ongoing legal requirements. Depending on the type of company, this may include registration issues, internal governance, employment policies, licensing, and state or federal compliance requirements.

A business lawyer helps you understand what applies to your company and what steps you need to take to stay on track.

- State and federal compliance guidance

- Business registrations and filings

- Employment-related policies and procedures

- Ongoing legal maintenance as your company grows

Avoid costly compliance issues—use the contact form or call (615) 747-7467 to schedule your consultation.

4. Protects Your Brand and Ideas

Your business name, branding, and original work can be some of your most valuable assets. A business lawyer can help you take steps to protect them.

- Trademark registration

- Brand protection strategy

- Guidance on intellectual property issues

- Help addressing misuse by competitors or others

Protecting your brand early can help you avoid conflicts and preserve the identity you are working hard to build.

Ready to protect your brand? Reach out through this page or call (615) 747-7467 to get started.

5. Helps Resolve Disputes

Even strong businesses can run into disagreements. These problems may involve partners, customers, vendors, employees, or other companies. A business lawyer helps you evaluate the issue, understand your options, and work toward a practical resolution.

This may include:

- Demand letters and negotiation

- Contract dispute analysis

- Business tort and commercial dispute guidance

- Litigation support when necessary

Dealing with a dispute? Contact Moore Law PC through the site or call (615) 747-7467 for guidance.

Do You Need a Business Lawyer?

Many business owners benefit from legal guidance long before there is a lawsuit or major problem. You may want to speak with a business lawyer if you are:

- Starting a new business

- Choosing between an LLC and a corporation

- Entering into contracts

- Bringing on a partner or investor

- Hiring employees or contractors

- Trying to protect a name, logo, or brand

- Facing a business dispute

- Planning for growth

Legal guidance is not just for emergencies. In many cases, it is one of the best ways to reduce risk and make better business decisions.

If you are unsure where to start, use the contact form or call (615) 747-7467 to schedule your initial consultation.

When Should You Hire a Business Lawyer?

The best time to hire a business lawyer is usually before you need one urgently. Working with a lawyer early can help you avoid common mistakes, save money over time, and build a stronger legal foundation.

Waiting until a problem becomes urgent often limits your options and increases the cost of fixing it.

Why Working with a Business Lawyer Matters

A business lawyer is not just someone to call when something goes wrong. The right lawyer can become a trusted advisor as your company grows, helping you make informed decisions, reduce legal exposure, and move forward with more confidence.

Start building your business on the right foundation—reach out through this page or call (615) 747-7467 today.

Start Your Business the Right Way

If you are ready to launch or strengthen your business, getting legal guidance early can make a real difference.

Use the contact form on this page or call (615) 747-7467 now to schedule your initial consultation.

Frequently Asked Questions

What does a business lawyer do in simple terms?

A business lawyer helps you start, run, and protect your business by handling legal matters such as formation, contracts, compliance, brand protection, and disputes.

Is a business lawyer necessary for an LLC?

A lawyer is not legally required to form an LLC, but working with one can help you choose the right structure, prepare proper documents, and avoid costly mistakes.

When should I hire a business attorney?

It is usually best to hire a business attorney before you sign important contracts, bring on partners, hire workers, launch a new venture, or face a dispute.

Can a business lawyer help with contracts?

Yes. A business lawyer can draft, review, revise, and negotiate contracts to help protect your interests and reduce the risk of future disputes.

Can a business lawyer help protect my brand?

Yes. Business lawyers often help with trademark registration, brand strategy, and other legal steps that protect the name and identity of your company.

About the Author — Nathan Moore, Attorney at Law

Nathan Moore is the founder of Moore Law PC, a business law firm based in Nashville, Tennessee. He has practiced law for more than twenty years, helping entrepreneurs and companies with trademark registration, business formation, contracts, and commercial disputes.

Have questions or need legal help? Use the contact form on this page or call (615) 747-7467 to schedule your initial consultation.